Assessment of the performance of the Bayesian Forecasting for Vector ARMA Processes

DOI:

https://doi.org/10.64060/JASR.v2i1.2Keywords:

Vector autoregressive moving average processes;, Bayesian forecasting, PredictionAbstract

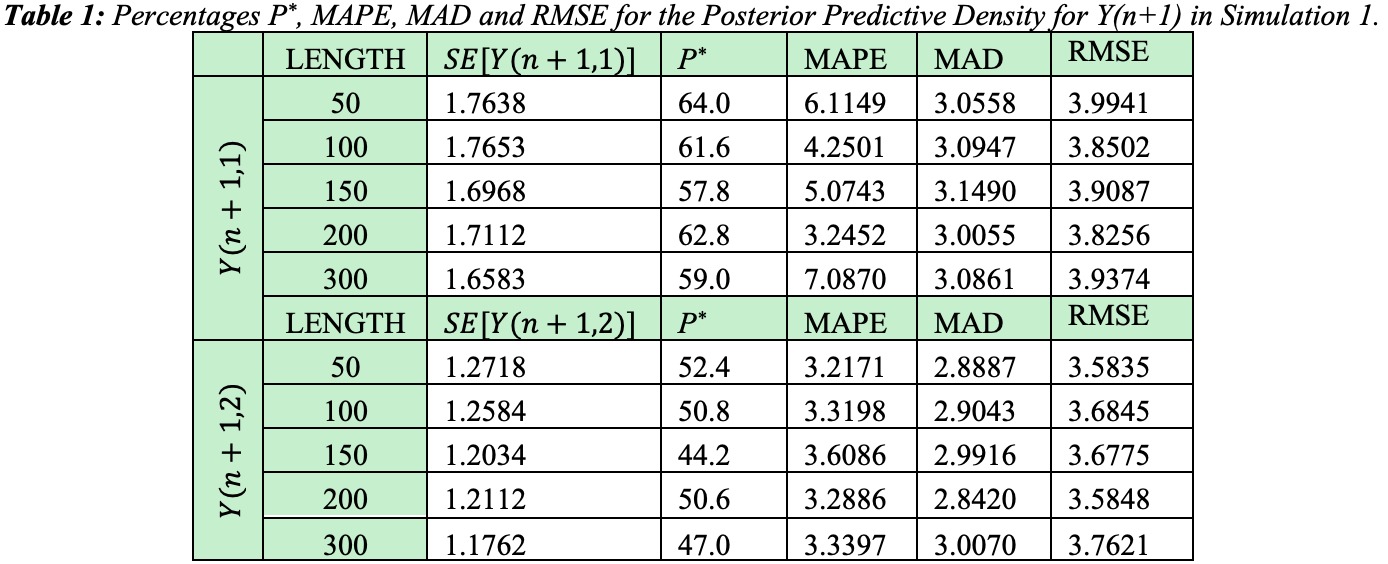

Multivariate time series are widely observed in numerous domains. In economics, for example, you can monitor the annual savings in conjunction with the real interest rate. Such variables are jointly analyzed to understand the dynamic interactions that exist between them, thus improving the precision of forecasts. Enhanced forecasting is achievable when the series are examined together, especially when one series holds information about another one. An approximate Bayesian analytical method to estimate and forecast vector autoregressive moving average (Vector ARMA) processes was introduced by Shaarawy (1989). A basic goal for the research in hand is the numerical assessment of the proposed approach in tackling forecasting difficulties associated with Vector ARMA processes through a comprehensive simulation study. Furthermore, the research checks how the performance of the suggested method fluctuates when varying parameter values and time series lengths. The findings of the numerical study demonstrated that the methodology was effective in accurately forecasting future observations for Vector ARMA processes across various values of the parameter and different time series lengths.

References

Albassam, M.S., Soliman E.E.A. and Ali, S.S. (2023). An Effectiveness Study of the Bayesian Inference with Multivariate Autoregressive Moving Average Processes. Communications in statistics- Simulation and Computation. 52(10):4773-4788. https://doi.org/10.1080/ 03610918.2021.1967986.

Ali, S.S. (2015). Bayesian Forecasting Of Vector Moving Average Processes. . The Egyptian Statistical Journal, 59(1), pp. (68-89). https://doi.org/10.21608/ESJU.2015.314457.

Amin, A. (2019). Gibbs Sampling for Bayesian Prediction of SARMA Processes. Pakistan Journal of Statistics and Operation Research. 15(2):483-499. https://doi.org/10.18187/ pjsor.v15i2.2174.

Box, G.E.P., Jenkins, G.M, Reinsel, G.C. and Ljung, G.M (2016). Time Series Analysis: Forecasting and Control (5th ed.). John Wiley & Sons.

Box, G. E. P., Tiao, G. C. (1973). Bayesian Inference in Statistical Analysis. Addison Wesley.

Broemeling, L., Shaarawy, S. (1988). Time series: A Bayesian analysis in time domain: Bayesian Analysis of Time Series and Dynamic Models. Studies in Bayesian Analysis of Time Series and Dynamic Models: (pp. 1–22). New York: Marcel Dekker Inc.

Brockwell, P. J. and Davis, R. A. (2016). Introduction to Time Series and Forecasting (3rd ed.). Springer.

Chan, J. C. and Eisenstat, E. (2015). Efficient estimation of Bayesian VARMAs with time-varying coefficients [Paper presentation]. 2015 CAMA Working Paper 19/2015. The Australian National University, Australia.

Chatfield, C. (2019). The Analysis of Time Series: Theory and Practice. An Introduction with R (7th ed.). Chapman & Hall.

Chib, S. and Greenberg, E. (1994). Bayes inference in regression models with ARMA (p, q) errors. Journal of Econometrics. 64(1-2):183-206. https://doi.org/10.1016/0304-076 (94)90063-9.

Cooley, T. F. and Dwyer, M. (1998). Business cycle analysis without much theory a look at structural VARs. Journal of Econometrics. 83(1-2):57–88. https://doi.org/10.1016/S0304-4076(97)00065-1.

Hall, A. D. and Nicholls, D. F. (1980). The evaluation of exact maximum likelihood estimates for VARMA models. Journal of Statistical Computation and Simulation. 10(3-4):251-262. https://doi.org/10.1080/00949658008810373.

Hillmer, S. C. and Tiao. G. C. (1979). Likelihood function of stationary multiple autoregressive moving average models. Journal of the American Statistical Association. 74(367):652-660. http://doi.org/10.1080/01621459.1979.10481666.

Kascha, C. (2012). A comparison of estimation methods for vector autoregressive moving -average models. Econometric Reviews. 31(3):297–324. https://doi.org/10.1080/07474938. 2011.607343.

Koop, G. (2013). Forecasting with Medium and Large Bayesian VARS. Journal of Applied Econometrics. 28(2):177-203. https://doi.org/10.1002/jae.1270.

Liu, L. M. (2009). Time Series Analysis and Forecasting (2nd ed.). Villa Park, IL: Scientific Computing Associates.

Lütkepohl. (2007). New Introduction to Multiple Time Series Analysis. Berlin: Springer.

Marriott, J., Ravishanker, N., Gelfand, A. and Pai, J. (1996). Bayesian analysis of ARMA processes: Complete sampling-based inference under full likelihoods. In Bayesian Statistics and Econometrics: Essays in honor of Arnold Zellner, D., Berry, K., Chaloner, and J., Geweke; (eds). New York: Wiley.

Mauricio, J. A. (1995). Exact maximum likelihood estimation of stationary vector ARMA models. Journal of the American Statistical Association. 90(429):282-291. https://doi.org/ 10.1080/01621459.1995.10476511.

Monahan, J. F. (1983). Fully Bayesian Analysis of ARIMA Time Series Models. Journal of Econometrics. 21(3):307–331. https://doi.org/10.1016/0304-4076(83)90048-9.

Newbold, P. (1973). Bayesian Estimation of Box and Jenkins Transfer Function Model for Noise Models. Journal of the Royal Statistical Society-Series B. 35(2):323-336.

Raghavan, M., Athanasopoulos, G. and Silvapulle, P. (2009). VARMA models for Malaysian Monetary Policy Analysis [Paper Presentation]. 2009 Monash University, Department of Econometrics and Business Statistics Working Papers, Malaysia.

Ravishanker, N., I. and Ray, B. K. (1997). Bayesian analysis of vector ARMA models using Gibbs sampling. Journal of Forecasting. 16(3):177–194. https://doi.org/10.1002/(SICI)1099-131X(199705)16:3%3C177::AID-FOR650%3E3.0.CO;2-%23.

Shaarawy, S.M. (l989). Bayesian Inferences and Forecasts with Multiple ARMA Models. Communications in Statistics-Theory and Methods. 18(4):1481–1509. https://doi.ord/ 10.1080/ 03610918908812836.

Shaarawy, S.M., Soliman, E.E.A. and Ali, S.S. (2007). Bayesian identification of moving average models. Communications in Statistics-Theory and Method. 36(12):2301-2312. https://doi.org/10.1080/03610920701215449.

Shaarawy, S.M. (2023). Bayesian modeling and forecasting of vector autoregressive moving average processes. Communications in Statistics-Theory and Method. 52(11):3795-3815. https://doi.org/ 10.1080/03610926.2021.1980047.

Shaarawy, S.M., Ali, S.S. and Soliman, E.E.A. (2024). Bayesian Identification of Seasonal Vector ARMA Processes. The Egyptian Statistical Journal, 68(2), pp. (129-145). https://doi.org/10.21608/esju.2024.318938.1044.

Shea, B. L. (1987). Estimation of multivariate time series. Journal of Time Series Analysis. 8(1):95-109. https://doi.org/10.1111/j.1467-9892.1987.tb00423.x

Tiao, G. C., Box, G. E. P. (1981). Modeling Multiple Time Series with Applications. Journal of the American Statistical Association. 76(376): 802–816. https://doi.org/10.1080/ 01621459.1981.10477728.

Tunnicliffe W. G. (1973). The estimation of parameters in multivariate time series models. Journal of the Royal Statistical Society-Series B. 35(1):76-85. https://doi.org/10.1111/j.2517-6161.1973.tb00938.x

Wei, W. W. S. (2005). Time Series Analysis: Univariate and Multivariate Methods (2nd ed.). Reading, MA: Addison Wesley.

Wei. W. W. S. (2019). Multivariate Time Series Analysis and Applications. John Wiley & Sons Ltd.

Zellner, A. (1971). An Introduction to Bayesian Inference in Econometrics. John Wiley and Sons, New York.

Zellner, A. and Reynolds, R. (1978, June 2-3). Bayesian Analysis of ARMA Models [Paper Presentation]. 1978 the Sixteenth Seminar on Bayesian Inference in Econometrics.

Downloads

Published

Issue

Section

License

Copyright (c) 2025 SCOPUA Journal of Applied Statistical Research

This work is licensed under a Creative Commons Attribution 4.0 International License.

How to Cite