Evaluating Nigeria Exchange Group All Share Index: Insights from Linear and GARCH Modeling Techniques

DOI:

https://doi.org/10.64060/JASR.v1i3.6Keywords:

All Share Index, GARCH Modeling, Linear Regression, Nigerian Exchange Group, Stock Market Volatility, Time Series AnalysisAbstract

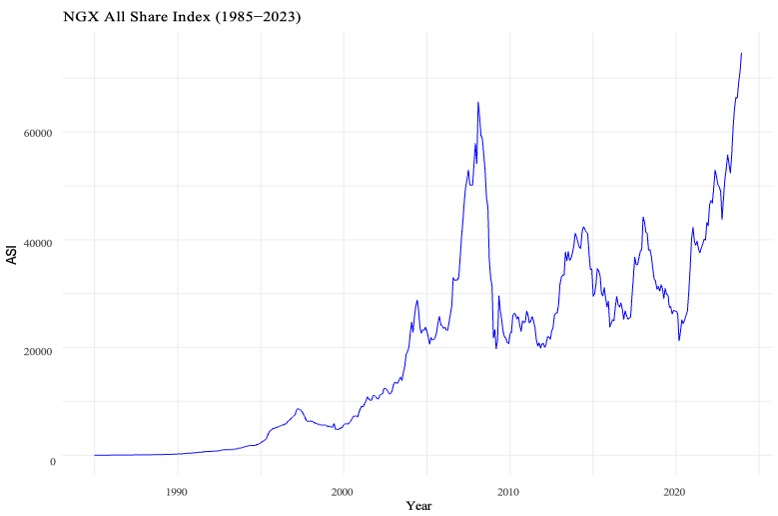

This study investigates the volatility of the Nigeria Exchange Group All Share Index (ASI) using linear regression and Generalized Autoregressive Conditional Heteroskedasticity (GARCH) modeling techniques. Despite prevalent public concerns regarding stock market instability, our analysis reveals that these perceptions are often exaggerated, driven largely by historical price levels and media representation. We employed a linear regression model to analyze monthly historical ASI data from 1985 to 2023, establishing a significant positive relationship between time and ASI values, with an R2 value of 0.7493, indicating that approximately 75% of the variance in ASI can be explained by the model. The Breusch-Godfrey test highlighted significant serial correlation in the residuals, necessitating further analysis using GARCH models to account for time-varying volatility. Our findings suggest that traditional asset pricing models may overlook alter- native risk measures that investors prioritize, emphasizing the need for a more nuanced understanding of market behavior. The adequacy of the model is achieved with a p-value 0.000017. Overall, this study contributes to the existing literature by offering insights into the dynamics of the Nigerian stock market and its volatility patterns, which are crucial for investors and policymakers alike.

References

[1] Michael O Nyong. “Capital market development and long-run economic growth: The- ory, evidence and analysis”. In: First Bank Review 4.1 (1997), pages 13–38.

[2] Obubu Maxwell, Obiora-Ilouno Happiness, Uzuke Chinwendu Alice, and Ikediuwa Udoka Chinedu. “An empirical assessment of the impact of Nigerian all share index, Market Capitalization, and Number of Equities on Gross Domestic Product”. In: Open Journal of Statistics 8.3 (2018), pages 584–602. URL: https://doi.org/%2010.4236/ ojs.2018.83038.

[3] G William Schwert. “Stock market volatility”. In: Financial analysts journal 46.3 (1990), pages 23–34. URL: https://doi.org/10.2469/faj.v46.n3.23.

[4] Richard T Baillie and Ramon P DeGennaro. “Stock returns and volatility”. In: Journal of financial and Quantitative Analysis 25.2 (1990), pages 203–214. URL: https:// doi.org/10.2307/2330824

[5] Hans R Stoll and Robert E Whaley. “Stock market structure and volatility”. In: The Review of Financial Studies 3.1 (1990), pages 37–71. URL: https://doi.org/10. 1093/rfs/3.1.37.

[6] Klaus Adam, Albert Marcet, and Juan Pablo Nicolini. “Stock market volatility and learning”. In: The Journal of finance 71.1 (2016), pages 33–82. URL: https://doi. org/10.1111/jofi.12364.

[7] Robert F Engle, Eric Ghysels, and Bumjean Sohn. “Stock market volatility and macroeconomic fundamentals”. In: Review of Economics and Statistics 95.3 (2013), pages 776–797. URL: https://doi.org/10.1162/REST_a_00300.

[8] Adrian R Pagan and G William Schwert. “Alternative models for conditional stock volatility”. In: Journal of econometrics 45.1-2 (1990), pages 267–290. URL: https://doi.org/10.1016/0304-4076(90)90101-X.

[9] G William Schwert. “Stock volatility in the new millennium: how wacky is Nasdaq?” In: Journal of Monetary Economics 49.1 (2002), pages 3–26. URL: https://doi.org/ 10.1016/S0304-3932(01)00099-X.

[10] G William Schwert. “Stock volatility during the recent financial crisis”. In: European Financial Management 17.5 (2011), pages 789–805. URL: https :// doi . org / 10 . 1111/j.1468-036X.2011.00620.x.

[11] Kingsley Ikechukwu Okere, Obumneke Bob Muoneke, and Favour Chidinma Onuoha. “Symmetric and asymmetric effects of crude oil price and exchange rate on stock mar- ket performance in Nigeria: Evidence from multiple structural break and NARDL analysis”. In: The Journal of International Trade & Economic Development 30.6 (2021), pages 930–956. URL: https://doi.org/10.1080/09638199.2021.1918223.

[12] Oluwatosin Adeniyi and Terver Kumeka. “Exchange rate and stock prices in Nigeria: Firm-level evidence”. In: Journal of African Business 21.2 (2020), pages 235–263. URL: https://doi.org/10.1080/15228916.2019.1607144.

[13] Shehu Usman Rano Aliyu. “Exchange rate volatility and export trade in Nigeria: An empirical investigation”. In: Applied Fi-nancial Economics 20.13 (2010), pages 1071– 1084. URL: https://doi.org/10.1080/09603101003724380.

[14] Godknows, I. M. (2024). Forecasting Nigerian Stock Market Volatilities using Bagging and Ensemble Averaging. CBN Journal of Applied Statistics, 15(2).

[15] Yuehchao Wu and Remya Kannan. Time Series Analysis of Apple Stock Prices Using GARCH models. Accessed: 2024-10-23. 2017. URL: https://rstudio-pubs-static. s3.amazonaws.com/258811_b43d4c7bb2c74851b5b95f29a09c5b30.html.

[16] Jukka Nyblom. “Testing for the constancy of parameters over time”. In: Journal of the American Statistical Association 84.405 (1989), pages 223–230. URL: https:// doi.org/10.1080/01621459.1989.10478759.

[17] Carlos M Jarque and Anil K Bera. “Efficient tests for normality, homoscedasticity and serial independence of regression residu-als”. In: Economics letters 6.3 (1980), pages 255–259. URL: https://doi.org/10.1016/0165-1765(80)90024-5.

[18] Greta M Ljung and George EP Box. “On a measure of lack of fit in time series models”. In: Biometrika 65.2 (1978), pages 297–303. URL: https://doi.org/10 . 1093/biomet/65.2.297.

[19] Adams, S. O. (2024). Asymmetric GARCH Type Models and LSTM for Volatility: Evidence from the Nigerian Stock Market. SSRN Preprint.

[20] Jarque, C. M., & Bera, A. K. (1987). A test for normality of observations and regression residuals. International Statistical Review / Revue Internationale de Statistique, 55(2), 163–172.

[21] Alfeus, M. (2025). Improving Realised Volatility Forecast for Emerging Markets.

[22] Adegboyo, O. (2025). Modelling and Forecasting of Nigeria Stock Market Volatility. SpringerOpen/FBJ.

[23] Draper, N.R. & Smith, H. (1998). Applied Regression Analysis (3rd ed.). Wiley.

[24] Engle, R. F. (1982). Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of United Kingdom Infla-tion. Econometrica, 50(4), 987–1007.

[25] Bollerslev, T. (1986). Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics, 31(3), 307–327.

[26] Chinedu, E. Q., & Obulezi, O. J. (2024). Optimizing GARCH Models for Financial Volatility. Risk Assessment and Manage-ment Decisions, 1(1), 62-74. URL: https://doi.org/10.48314/ramd.v1i1.31

[27] Chinedu, E. Q., Asogwa, E. C., Sunday, B. T., Onyeizu, N. M., & Obulezi, J. O. (2023). Unraveling emotions: contemporary approaches in sentiment analysis. J Sen Net Data Comm, 3(1), 223-230.

Downloads

Published

Issue

Section

License

Copyright (c) 2025 SCOPUA Journal of Applied Statistical Research

This work is licensed under a Creative Commons Attribution 4.0 International License.

How to Cite